Millions of older adults are opening their mail this year to find unexpected shifts in their healthcare coverage, making the 2026 Medicare Advantage changes a critical financial and medical event. If you rely on a Medicare Advantage plan, you might experience shrinking provider networks, reduced extra benefits, and changing out-of-pocket limits. Insurance carriers are adjusting to new federal funding rules and rising healthcare costs, which directly affects your bottom line. You must proactively evaluate your healthcare options to ensure your preferred doctors remain in-network and your prescription drugs remain affordable. Staying informed empowers you to navigate these plan changes confidently, protect your health, and secure the most cost-effective medical coverage for the upcoming year.

Understanding the Basics: What Is Happening to Medicare Advantage in 2026?

To understand your healthcare coverage in 2026, you first need to grasp how Medicare Advantage operates. Medicare Advantage, also known as Medicare Part C, functions as a private alternative to Original Medicare. When you enroll, a private insurance company administers your Part A hospital and Part B medical benefits. Most plans bundle in Part D prescription drug coverage and entice you with extra perks. The federal government pays these private insurers a set amount monthly to manage your care.

In 2026, the landscape shifted because federal regulators adjusted the formulas used to pay these private companies. Regulators implemented changes designed to control government spending and ensure the long-term solvency of the Medicare program. As a result, insurance carriers are receiving tighter federal reimbursements. Because these companies operate on profit margins, they must adjust their plan offerings to compensate for the reduced influx of federal dollars. You directly feel the impact of these financial recalculations [4].

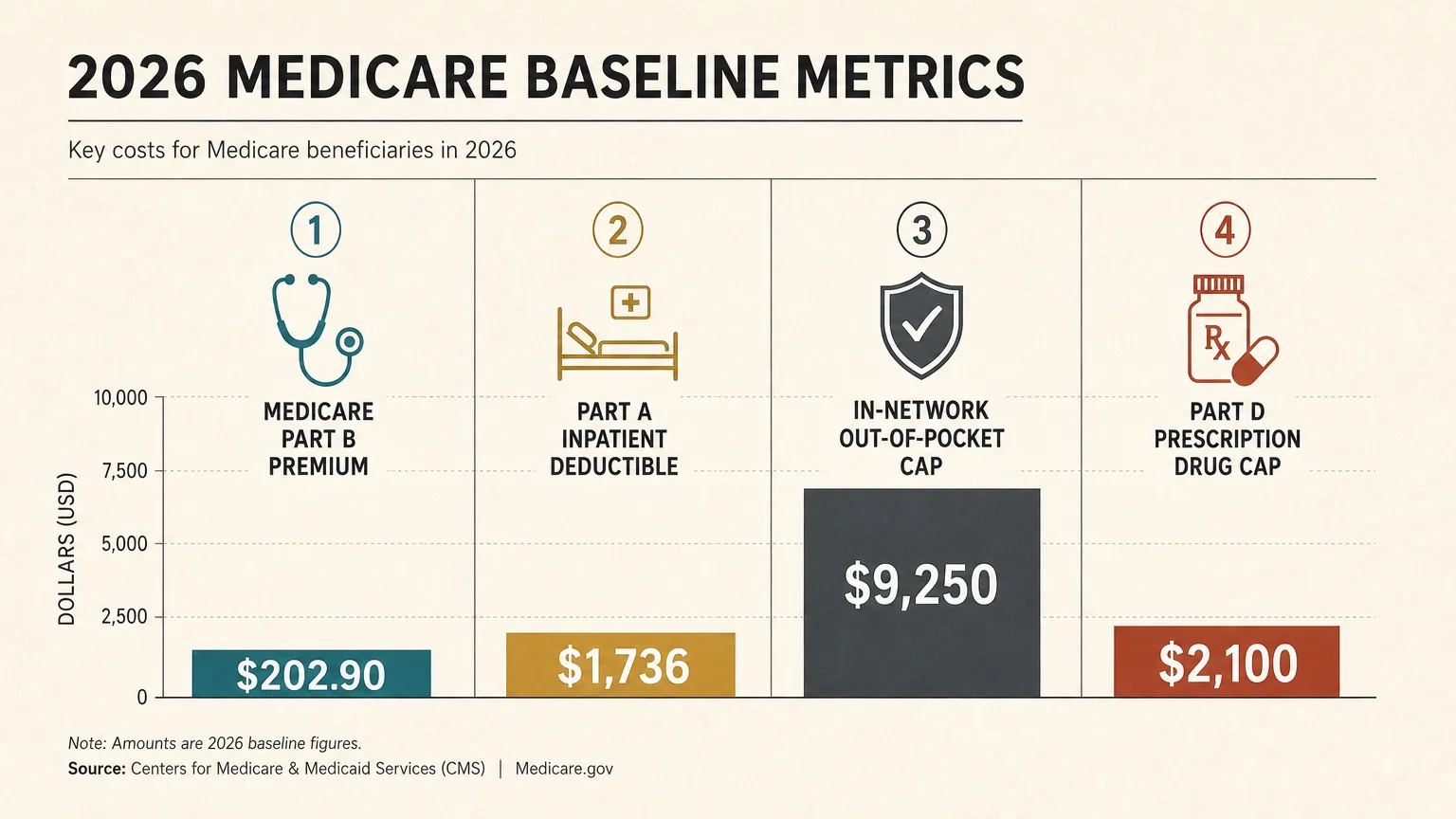

The baseline financial metrics for healthcare have also increased across the board. The standard Medicare Part B premium has risen to $202.90 per month, and the Part A inpatient hospital deductible now stands at $1,736 [3]. These baseline figures influence how much you ultimately pay out of pocket. Insurance companies factor these rising costs into their plan designs, often passing the burden onto you through higher copayments.

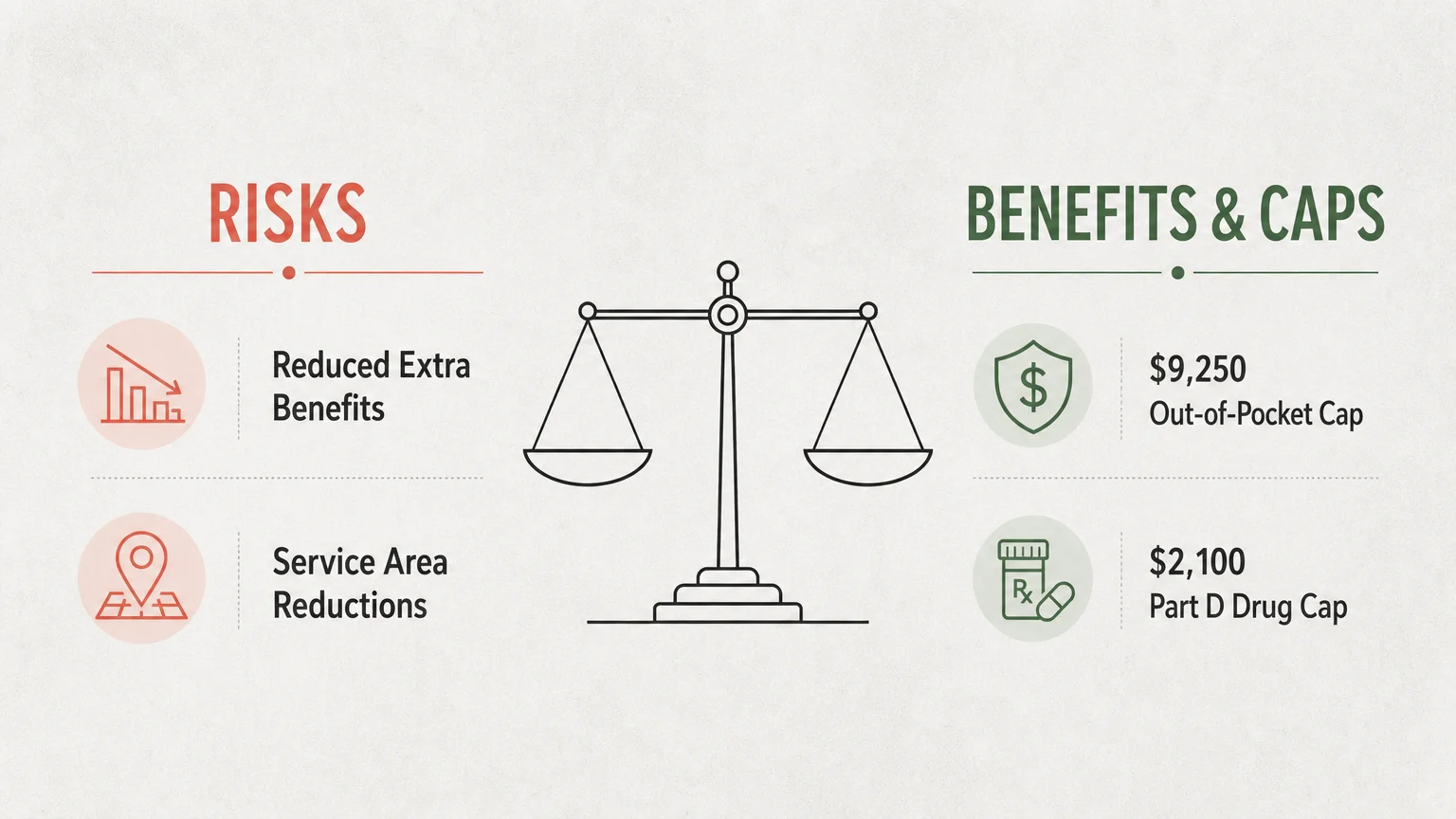

The federal government slightly lowered the maximum allowable out-of-pocket cap for in-network services to $9,250 in 2026 [7]. While a decrease sounds positive, reaching a $9,250 threshold remains financially devastating for retirees on a fixed income. Furthermore, the out-of-pocket cap for Part D prescription drugs remains a vital safety net, limiting your catastrophic medication expenses to roughly $2,100 for the year [3]. Understanding these moving parts is essential because the plan you loved might look completely different when the calendar turns.

Key Considerations for Seniors Facing Coverage Shifts

As you age, your healthcare needs naturally become more complex, making these 2026 plan changes deeply personal. Older adults typically manage multiple chronic conditions, which requires building a trusted team of medical specialists over many years. When a Medicare Advantage plan alters its provider network to save money, your long-standing relationship with a cardiologist or an oncologist is immediately threatened. If your preferred doctor is dropped from the network, you must either pay exorbitant out-of-network fees or undergo the stressful process of finding a new specialist.

Another major consideration involves the alarming increase in Service Area Reductions. Some insurance carriers are completely withdrawing their Medicare Advantage plans from specific counties because those regions are no longer profitable [2]. If you live in an affected area, you will receive a termination notice stating that your plan will cease to exist. This situation forces millions of seniors into a chaotic scramble during the Annual Enrollment Period. You cannot simply ignore the mail; you must take immediate action to secure a new insurance policy.

Living on a fixed income further magnifies the impact of these coverage shifts. When retirees map out their monthly budgets, they account for every predictable expense. In 2026, many plans are increasing the daily copayments required for inpatient hospital stays. An unexpected illness could quickly derail your financial stability if your plan now requires a massive daily copay for a hospital admission.

The erosion of extra benefits represents another painful reality. Seniors flocked to Medicare Advantage plans primarily because of the generous allowances for over-the-counter pharmacy items, groceries, and comprehensive dental care. Facing severe financial constraints, insurers are drastically scaling back these perks [2]. The quarterly grocery card that helped you manage food inflation might be reduced or completely eliminated. Relying on these extra benefits to balance your household budget is no longer a safe strategy.

Benefits and Potential Risks of the 2026 Landscape

Despite the challenging financial environment, the 2026 Medicare Advantage changes introduce several distinct benefits. One significant positive change involves the restructuring of cost-sharing for behavioral health services [7]. Federal regulations now mandate that Medicare Advantage plans must match or improve upon the cost-sharing structures found in Original Medicare for mental health and substance use disorder treatments. If you require regular therapy sessions, you will no longer face artificially inflated copayments, removing a massive barrier to achieving mental wellness.

Prescription drug affordability also sees continued protections. The cost of insulin remains strictly capped at $35 per month, and importantly, no deductible applies to these life-saving purchases [7]. Additionally, the automatic renewal feature for the Medicare Prescription Payment Plan ensures that you can spread your out-of-pocket medication costs into predictable, budget-friendly monthly installments without jumping through administrative hoops every single year [7].

However, the potential risks embedded in the 2026 plans warrant your immediate attention. The most dangerous risk is the aggressive expansion of prior authorization requirements [2]. To control internal costs, insurance companies increasingly force doctors to obtain corporate approval before proceeding with necessary surgeries, diagnostic imaging, or expensive treatments. These administrative hurdles routinely cause dangerous delays in medical care. You could find yourself waiting weeks for an insurance clerk to approve an MRI.

Shrinking provider networks present another massive risk to your physical health. Insurers are deliberately narrowing their networks, terminating contracts with expensive hospital systems to preserve their profit margins. You must carefully verify whether the top-tier medical facilities in your region are still participating in your specific plan. A zero-dollar monthly premium offers zero value if it restricts you from accessing the best medical care when a life-threatening illness strikes. You must actively weigh these undeniable risks against the heavily advertised benefits.

What the Experts Say About Managing Your Healthcare

Medical professionals and health policy experts consistently warn that stability in your health coverage is intrinsically linked to better long-term health outcomes. Frequent disruptions in insurance often force patients to skip routine screenings, delay refilling essential medications, or abandon trusted physicians. Research shows that older adults who experience sudden interruptions in their continuum of care face a significantly higher risk of preventable hospitalizations. Experts urge you to prioritize plans that offer stability over plans that simply offer flashy temporary perks.

Leading public health authorities emphasize the critical nature of preventative medicine. Guidance from the Centers for Disease Control and Prevention highlights how consistent medical oversight is required to effectively manage chronic illnesses like diabetes and heart disease. If a 2026 plan change removes your access to the endocrinologist who has successfully managed your health for a decade, your long-term prognosis could be severely compromised. Maintaining your physician relationships should remain your primary metric when evaluating insurance options.

Comprehensive medical research supports the urgent need for timely interventions without administrative delays. Institutions such as the National Institutes of Health fund studies demonstrating that early detection and rapid treatment protocols yield the most favorable prognoses for aggressive diseases. The increasing reliance on prior authorizations by Medicare Advantage plans directly contradicts this medical consensus, as corporate financial algorithms should never override clinical judgment.

Patient advocacy organizations are becoming increasingly vocal about the deceptive nature of insurance marketing. They warn that glossy brochures aggressively promote free gym memberships while intentionally burying the severe limitations of their provider networks. Advocates recommend that you completely ignore the marketing noise. Instead, focus exclusively on the raw data: the maximum out-of-pocket limit, the specific copayments for specialist visits, and the strictness of the medication formulary. You must become a defensive consumer in a market designed to maximize corporate profits.

Practical Steps and Actionable Advice for Open Enrollment

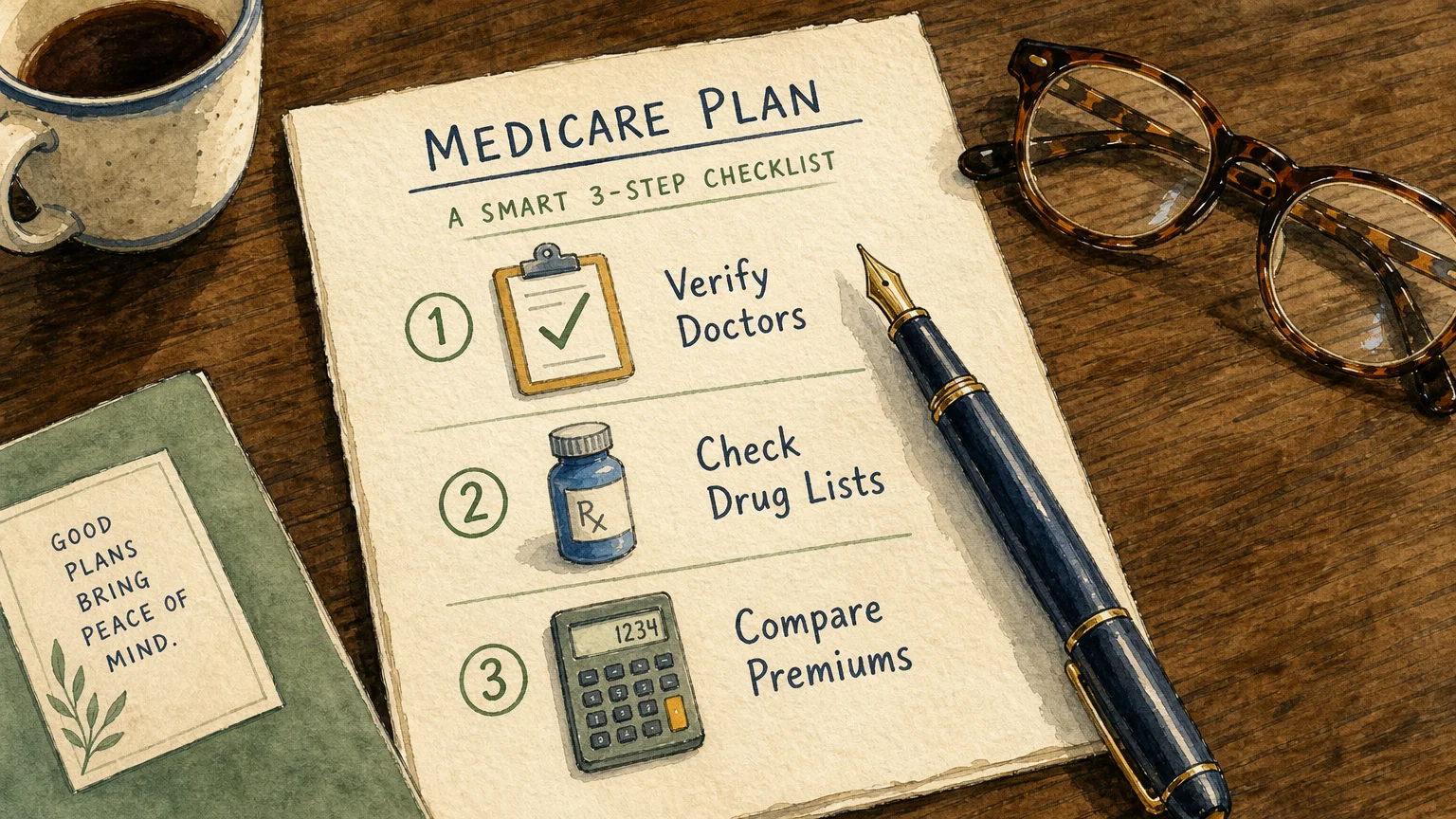

The very first action you must take is to locate and thoroughly read your Annual Notice of Changes document [8]. Your insurance company is legally required to send this document to you every September. Sit down with a notepad and explicitly document any increases to your maximum out-of-pocket limit, changes to your daily hospital copayments, and reductions in your extra benefits. This document is your blueprint for understanding exactly how your financial exposure will change in the upcoming year.

You must independently verify that your doctors are remaining in your plan’s network. Never rely solely on the insurance company’s online provider directory, as these databases are notoriously inaccurate. Instead, take the proactive step of calling your primary care physician and specialists directly in October. Speak to the billing department and explicitly ask if they are contracted to accept your exact Medicare Advantage plan for 2026. Making these phone calls can save you thousands of dollars in surprise medical bills.

Scrutinizing your prescription drug coverage is equally critical. Make a comprehensive list of every medication you currently take, including the exact dosage. Log onto the official federal Medicare website and use their plan finder tool to input your drugs. The tool calculates your estimated annual out-of-pocket costs across different plans. Pay close attention to formulary tier changes; an insurance company might move your generic blood pressure medication to a highly expensive tier.

Consider enlisting the expertise of a licensed, independent health insurance broker. Unlike captive agents working for one corporation, independent brokers can show you policies from multiple competing carriers. Their services are completely free to you. A knowledgeable broker can help you cut through confusing industry jargon, identify plans covering your specific doctors, and ensure you do not miss critical enrollment deadlines.

Frequently Asked Questions About 2026 Plan Changes

Why is my Medicare Advantage plan dropping my extra benefits?

Your insurance company is dropping extra benefits because the federal government has tightened the payment formulas used to fund these private plans in 2026. Faced with receiving less money per enrollee and battling rising overall medical costs, private insurers must cut their own expenses to maintain profit margins. Unfortunately, the easiest way for them to save money is to slash the allowances for dental care, vision hardware, and over-the-counter pharmacy cards that originally attracted you to the plan.

Will my prescription drug costs go up in 2026?

Your overall prescription drug costs will depend heavily on the specific medications you take, though the system has implemented new safety nets. While the out-of-pocket cap limits your catastrophic spending to around $2,100 for the year, your individual monthly premiums and specific copayments could still increase. Insurance companies frequently reorganize their drug formularies, moving medications into more expensive pricing tiers. You must manually check your specific prescriptions against your plan’s 2026 formulary to determine your actual daily costs.

What happens if my Medicare Advantage plan is discontinued entirely?

If your insurance company decides to pull your plan from your specific county or state, you will be subjected to a Service Area Reduction. You will receive an official notification letter stating that your coverage will end on December 31st. You will then be granted a Special Enrollment Period, giving you a dedicated window of time to select a new Medicare Advantage plan or transition back to Original Medicare without facing an immediate lapse in your medical coverage.

Can I easily switch back to Original Medicare if I am unhappy?

You can switch back to Original Medicare during the Annual Enrollment Period or the Medicare Advantage Open Enrollment Period from January through March [5]. However, returning is only half the battle. If you want to purchase a Medigap policy to cover the remaining twenty percent of your medical bills, you will likely have to pass strict medical underwriting. If you have preexisting health conditions, the company can legally deny your application.

Does the new out-of-pocket prescription cap apply to all plans?

Yes, the maximum out-of-pocket cap for prescription drugs applies to the Part D component of your medical coverage. Because the vast majority of Medicare Advantage plans include integrated Part D prescription drug coverage, this federal cap will protect you. Once your out-of-pocket spending on covered formulary drugs reaches the designated limit for 2026, the insurance company will cover one hundred percent of the costs for your approved medications for the remainder of the calendar year.

Conclusion and Final Thoughts

Navigating the 2026 Medicare Advantage changes requires diligence, patience, and a willingness to advocate for your own healthcare needs. The era of simply allowing your medical coverage to automatically renew without a second thought has ended. As insurance carriers aggressively adjust their provider networks, restrict extra benefits, and implement strict prior authorization rules, you must remain vigilant to protect your well-being. Take the time to review your Annual Notice of Changes, verify the participation of your physicians, and analyze your prescription drug costs. By staying informed, you can confidently weather these industry shifts and secure the optimal health coverage you deserve.

This article is intended for informational and educational purposes only and is not a substitute for professional medical advice, diagnosis, or treatment. Always consult with a qualified healthcare provider regarding any health concerns or before making any decisions related to your health or treatment.