Managing your healthcare budget starts with recognizing that prices for the top 25 prescription drugs are rising rapidly in the U.S., directly impacting your out-of-pocket expenses. Staying informed about skyrocketing medication prices allows you to make strategic choices regarding your Medicare coverage and pharmacy options before you face financial hardship. The pharmaceutical landscape is shifting; brand-name medications used to treat conditions like diabetes, heart disease, and autoimmune disorders are seeing unprecedented price hikes. For seniors relying on fixed incomes, navigating these rising drug costs often feels overwhelming. By understanding the driving forces behind these increases and learning how to find reliable alternatives, you can protect your financial stability while maintaining access to critical treatments.

Understanding the Basics

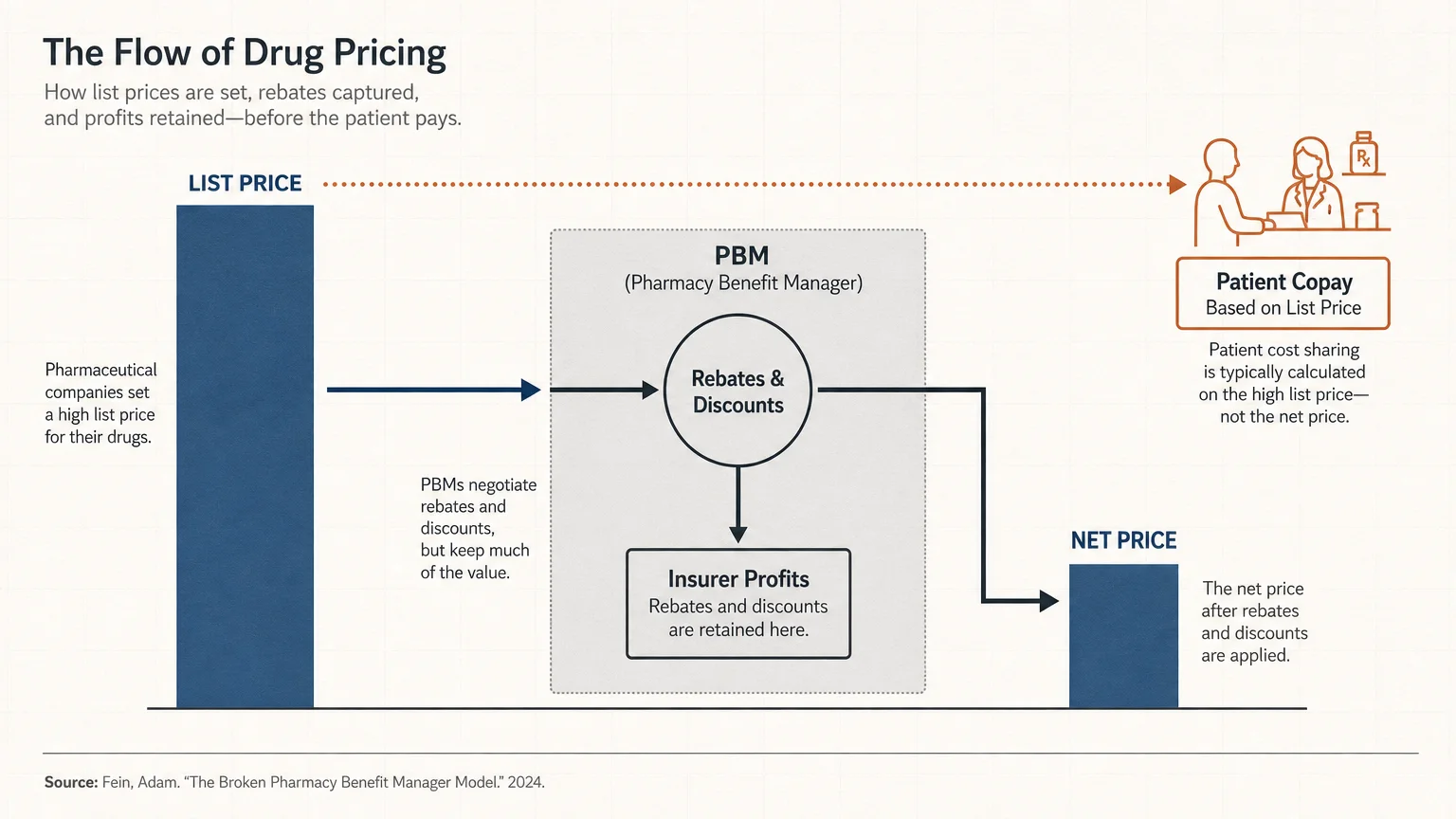

The pharmaceutical market operates on a complex pricing model that often leaves patients thoroughly confused and financially drained. When we examine the top twenty-five most prescribed medications in the nation—ranging from essential blood thinners and modern diabetes injectables to specialty treatments for severe autoimmune disorders—we see a consistent pattern of year-over-year price inflation. Pharmaceutical manufacturers set what is known as a list price, which serves as the official baseline cost of the drug before any discounts or rebates are applied. While your insurance company negotiates a much lower net price behind closed doors, your out-of-pocket copayments or deductibles are frequently calculated based on that artificially inflated list price.

You might wonder why a medication you have taken for years suddenly costs significantly more today. Pharmaceutical companies often cite the enormous costs of scientific research and development as the primary justification for these rapid price hikes. However, industry analysts frequently point out that many of the drugs experiencing the steepest increases are older medications that have already recouped their initial development costs multiple times over. Instead, companies utilize legal maneuvers called patent thickets; they add dozens of secondary patents to a single drug to prevent cheaper generic competitors from entering the market. By actively extending their monopoly over a specific treatment, manufacturers can continue to raise prices without fear of losing market share.

The role of Pharmacy Benefit Managers—often referred to as PBMs—adds another thick layer of complexity to prescription costs. These corporate middlemen are hired by insurance companies to negotiate prices with manufacturers and build the formularies you receive from your health plan. PBMs secure massive financial rebates in exchange for placing specific expensive drugs on preferred tiers. Unfortunately, those secretive rebate savings are rarely passed directly to you at the pharmacy counter. Instead, you pay a higher out-of-pocket cost based on the full list price, effectively subsidizing the rebates that pad the profits of these intermediaries. Understanding this opaque system is your first critical step toward recognizing why your healthcare expenses keep climbing.

Key Considerations for Seniors

Aging brings a unique set of physiological changes that make rising prescription drug costs a uniquely critical issue. As you grow older, your body naturally requires more medical support to manage chronic conditions such as hypertension, severe osteoporosis, and type 2 diabetes. This biological reality frequently leads to polypharmacy, a clinical term describing the simultaneous use of multiple prescription medications by a single patient. When you manage five or six different prescriptions every single month, a modest price increase on just two or three of those drugs can rapidly devastate a carefully planned monthly budget.

Relying on a fixed income leaves very little margin for error when healthcare expenses surge unexpectedly. When prescription drug prices rise faster than the annual cost-of-living adjustments provided by Social Security, your purchasing power inevitably shrinks. This acute financial squeeze can push you into dangerous territory, prompting medication non-adherence. You might find yourself occasionally skipping doses, splitting your pills in half, or delaying necessary monthly refills simply to stretch your budget until the next pension check arrives. This behavior, while completely understandable from a financial perspective, severely compromises your physical health and drastically increases the likelihood of costly hospitalizations down the road.

Medicare Part D provides essential coverage but features complex spending phases that can trigger sudden financial shock. For years, seniors feared the notorious coverage gap, where out-of-pocket costs temporarily spiked once a specific spending threshold was reached. While recent legislative changes have worked to close this gap and restructure out-of-pocket maximums, the underlying high list prices of top-tier brand-name drugs still translate to significant coinsurance burdens. If you require specialty medications for conditions like rheumatoid arthritis or certain forms of cancer, you might still face massive annual out-of-pocket costs before comprehensive catastrophic coverage kicks in. Navigating these coverage phases requires intense vigilance and a thorough understanding of how your specific plan prices your necessary treatments.

Benefits and Potential Risks

Navigating the treacherous waters of rising drug costs means actively exploring strategies designed to reduce your monthly pharmacy bills. Exploring these cost-saving measures offers substantial benefits, primarily by alleviating acute financial stress and freeing up resources for other essential daily needs like healthy food and safe housing. Switching from an expensive brand-name medication to a generic equivalent is one of the most highly effective ways to slash your expenses. The immediate benefit is purely economic; generic drugs often cost up to eighty-five percent less than their brand-name counterparts while delivering the exact same therapeutic effect. Lower prices ensure you can maintain continuous treatment for your chronic conditions without draining your retirement accounts.

However, these cost-saving strategies do not exist without their own distinct risks and everyday challenges. When switching to a generic medication, you must be aware that while the active chemical ingredient remains identical, the inactive ingredients—such as chemical dyes and dietary binders—can vary between different manufacturers. Yet, if you possess specific allergies to certain dietary fillers, a new generic formulation could potentially trigger an adverse physical reaction. Furthermore, retail pharmacies frequently switch their generic suppliers based on wholesale pricing, meaning the physical appearance of your pills might change from month to month, thereby increasing the risk of dangerous dosage confusion for older adults managing multiple pill bottles.

Another popular approach involves seeking out patient assistance programs or utilizing digital discount pharmacy cards to bypass your insurance altogether. The primary benefit is accessing steep cash discounts that sometimes beat your standard Medicare copayments, allowing you to secure vital medications for a fraction of the original cost. The downside is that money spent using third-party discount cards entirely outside of your insurance network will not count toward your Medicare Part D annual out-of-pocket deductible. Additionally, turning to international online pharmacies for cheaper imports carries profound safety risks, as these unregulated foreign channels frequently distribute counterfeit, expired, or improperly stored medications that could severely jeopardize your physical health.

What the Experts Say

Leading medical researchers and prominent health organizations highlight the severe public health crisis created by unchecked prescription drug inflation. Experts at the National Institutes of Health regularly publish data demonstrating the direct correlation between high out-of-pocket medication costs and poor clinical outcomes. Their extensive research confirms that when drug prices become completely unmanageable, patient adherence plummets. This forced non-adherence inevitably leads to exacerbated disease states, accelerated functional decline, and an increased rate of costly emergency room visits. Medical professionals strongly argue that a modern medication is entirely useless if the patient sitting in the doctor’s office cannot afford to purchase it at the local pharmacy. The medical consensus dictates that financial toxicity is a critical side effect requiring immediate intervention.

Advocacy groups heavily focused on aging populations continually lobby lawmakers to address structural flaws in the modern pharmaceutical market. These established organizations stress that the heavy financial burden falls disproportionately on older Americans, who consume a vastly higher volume of prescription medications than younger demographics. Respected experts advocate for increased governmental negotiation power and much stricter regulatory oversight regarding how manufacturers exploit existing patent laws. They argue that creating a highly transparent, tightly regulated pricing system is an urgent moral imperative necessary to protect the physical well-being of millions of vulnerable seniors across the nation.

Clinical practitioners from renowned institutions like the Mayo Clinic strongly urge older patients to become active, highly vocal participants in their own healthcare economics. They recommend breaking the outdated stigma and silence that often surrounds personal financial struggles. Doctors report they frequently write prescriptions for newer, heavily marketed drugs simply out of clinical habit, completely unaware of the massive financial burden those specific medications place on their older patients. Health experts advise that having transparent, profoundly honest conversations with your prescribing physician about budget constraints is crucial. Doctors can often recommend older, equally effective alternative medications that cost a mere fraction of the original price, or provide invaluable sample packages to help bridge a temporary coverage gap.

Practical Steps and Actionable Advice

Taking direct control of your healthcare expenses requires a proactive approach and a strong willingness to ask difficult questions. The very first action you should take is scheduling a comprehensive medication review with your primary care physician or a licensed clinical pharmacist. Bring every single pill bottle, daily vitamin, and herbal supplement you currently take to this dedicated appointment. Ask your doctor if every single prescription is still medically necessary; sometimes, seniors remain on medications for years after the original acute condition has fully resolved. For the drugs you absolutely must continue taking, directly ask your provider if there is a cheaper generic equivalent or an alternative medication within the same therapeutic class that treats the condition effectively. State clearly that you are actively looking for reliable ways to reduce your monthly pharmacy bill.

Reviewing your Medicare Part D or Medicare Advantage coverage during the annual open enrollment period is an absolutely vital financial strategy. Insurance companies change their formularies—the extensive lists of covered drugs—every single year. By logging onto the official federal Medicare website and inputting your specific list of daily prescriptions, you can accurately compare estimated annual out-of-pocket costs across dozens of different plans available in your local zip code. Switching to a new health plan that offers vastly superior coverage for your specific regimen can save you hundreds, if not thousands, of dollars annually.

Exploring alternative fulfillment methods can also yield highly significant daily savings. Check the standard cash price of your medications using reputable digital pharmacy discount platforms before automatically handing over your insurance card at the retail counter. Additionally, consider transitioning your chronic, daily medications to a verified mail-order pharmacy. Many modern insurance plans offer substantial financial discounts—such as providing a full ninety-day supply for the price of a standard sixty-day supply—if you utilize their preferred home delivery service. Finally, investigate whether you clearly qualify for State Pharmaceutical Assistance Programs or federal low-income subsidy programs, which provide direct financial assistance to seniors struggling to afford medical treatments.

Frequently Asked Questions

Why do prescription drugs cost so much more in the U.S. than in other countries?

The United States notably lacks a centralized, governmental body that regulates or negotiates drug prices on a national scale. In many other highly developed nations, the federal government operates as a single-payer system, fully leveraging the massive purchasing power of the entire country to negotiate strict price caps directly with pharmaceutical manufacturers. In the U.S., the heavily fragmented healthcare system relies on thousands of individual insurance plans to negotiate completely separately, severely diluting their collective bargaining power and actively allowing drug companies to set much higher initial list prices without immediate regulatory pushback.

Will the recent Medicare legislative changes actually lower my pharmacy bills?

Recent federal legislation has introduced several new mechanisms designed to curb out-of-pocket costs specifically for Medicare beneficiaries. These vital changes include officially capping the monthly cost of vital insulin and completely restructuring Part D to include a strict annual out-of-pocket maximum that provides massive financial relief for seniors requiring expensive specialty drugs. Additionally, the federal government has formally gained the unprecedented authority to negotiate prices for a select number of the highest-spending drugs. While these progressive changes offer tremendous financial relief, they currently roll out gradually over several years. You must still diligently review your individual coverage annually.

Are generic medications truly as effective as expensive brand-name drugs?

Yes, federal regulators strictly require generic medications to have the exact same active chemical ingredients, clinical strength, dosage form, and approved route of administration as the original brand-name product. Generics must also successfully prove bioequivalence, meaning they absorb into the human bloodstream and act upon the body in the exact same reliable manner as the original drug. The primary differences lie entirely in inactive ingredients, such as basic flavorings and visual dyes, which do not alter therapeutic performance whatsoever. For the vast majority of conditions, switching to a generic provides identical clinical results while offering substantial financial savings.

How can I find out if I qualify for extra help paying for my prescriptions?

The federal Social Security Administration proudly offers a robust low-income subsidy program commonly referred to as Extra Help. This excellent program directly assists Medicare beneficiaries who have strictly limited income and resources in paying for their Part D premiums, annual deductibles, and regular copayments. You can safely apply directly through the official government Social Security website or by calling their national toll-free number. Even if you do not qualify for federal assistance, explore State Pharmaceutical Assistance Programs immediately, as many individual states offer their own supplemental health grants and unique discount programs to help resident seniors afford daily medications.

Securing Your Financial and Physical Health

Navigating the relentless surge in prices for the top 25 prescription drugs heavily requires constant vigilance, thorough education, and highly proactive communication with your medical team. As pharmaceutical costs actively continue to outpace normal inflation, fiercely protecting your financial stability is just as vitally important as diligently managing your physical health. You inherently possess the power to directly combat these rising expenses by questioning the pricing status quo, safely exploring generic medical alternatives, fully optimizing your Medicare coverage annually, and eagerly utilizing available financial assistance programs. Do not let the massive complexity of the modern healthcare system intimidate you into paying more than is necessary. By taking deliberate, highly informed actions today, you can successfully manage your healthcare expenses and boldly ensure you maintain uninterrupted access to the essential medications that support your daily independence and overall vitality.

This article is intended for informational and educational purposes only and is not a substitute for professional medical advice, diagnosis, or treatment. Always consult with a qualified healthcare provider regarding any health concerns or before making any decisions related to your health or treatment.